Let Me Get This Strait

Polymarket’s Strait of Hormuz contracts show what happens when you define the rules mid-game, writes Ryan Adler, Superforecaster and Good Judgment Question Team Lead.

I previously wrote about how badly Polymarket framed its US “invasion” of Venezuela, but now we have a new standard for how not to write a series of event contracts.

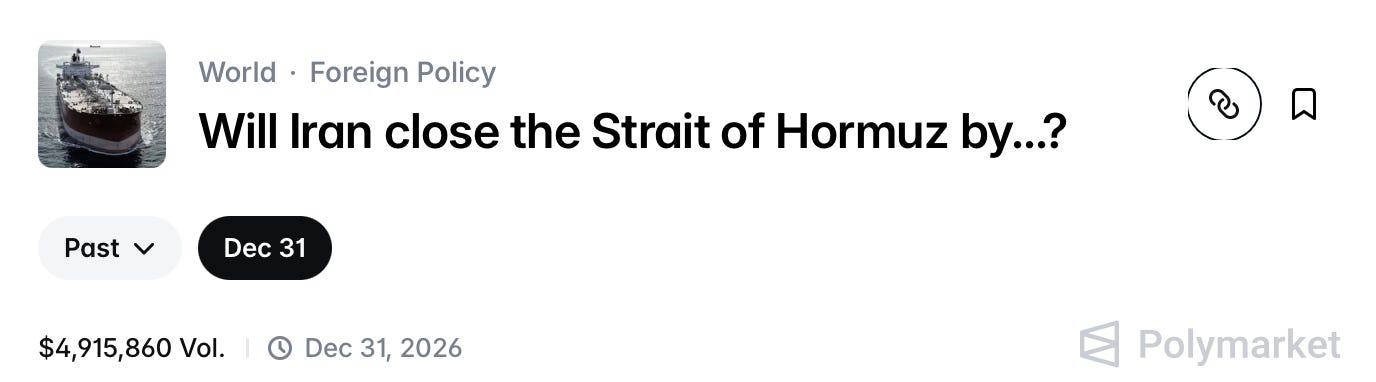

“Will Iran close the Strait of Hormuz by...?”

Created on 20 January 2026, the original rules were oddly scant on particulars, simply asking whether “Iran halts or severely restricts international maritime traffic through the Strait of Hormuz.” That might seem simple enough to a casual reader who may or may not be able to find the Strait of Hormuz on a map, but if ambiguity were trees, this might as well be called Oregon.

The standard isn’t quantified in any appreciable way. What does “severely restricts” mean? If 2026 were a sequel to 2025, nobody would care because there would be no reason to inquire further. However, hundreds of planes hitting a thousand targets in short order have turned attention to this very fuzzy threshold.

Making up rules as you go

On 1 March 2026, the powers that be at Polymarket decided it was time to think through their terms:

“Per the rules, this market requires Iran to halt or severely restrict international maritime traffic through the Strait of Hormuz. “Severely restrict” will be defined as a [sic] 80% or greater decrease in the 7 day moving average of commercial vessel transits (both cargo and tanker ships) on a given date when compared to the seven-day moving average 30 days prior, as reported by the IMF’s PortWatch service (see: https://portwatch.imf.org/pages/cb5856222a5b4105adc6ee7e880a1730), with the decrease being directly caused by actions taken by the Iranian regime. A consensus of credible reporting or government sources confirming that Iran has halted maritime traffic through the Strait of Hormuz will also qualify.”

PortWatch is awesome. As someone constantly on the lookout for new sources of data, I was moderately giddy when it first came online. But if you’re going to use it, you’ve got to call it out from the start. This is akin to starting an NFL game and waiting until the second quarter to define penalties.

Making up standards as you go does a disservice to market participants and to anyone looking for “accurate, unbiased forecasts.” What good is a forecast if you don’t know exactly what you’re forecasting?

No peanuts

However, the issues don’t end there. In the new rules made up during the second quarter, Polymarket went from “If Iran halts or severely restricts” to the “decrease being directly caused by actions taken by the Iranian regime.” What does “directly” mean?

Soon after the bombs started dropping, sea vessel insurers started canceling policies for ships in the region. While they were prompted by the beginning of hostilities, would this count as a decrease being directly caused by Iran? If all of the insurers effectively block vessels from crossing the Strait of Hormuz with or without Iran firing a shot, does that count?

We could play the “proximate cause” vs “but-for cause” game, with the latter arguably meaning that George Washington Carver is responsible. (He perfected the manufacture of peanut oil, which Rudolph Diesel used to fuel his new engine, which created the vast global market for diesel fuel, which drives the importance of exports through the Strait of Hormuz to this day…but I digress.) But is Iran necessarily the direct cause? Maybe they’ll figure that out by the end of the third quarter.

That millions of dollars in contracts trade on such inherently bad terms is befuddling to me, and that they haven’t decided to take the time to figure out what they’re doing should raise more red flags for traders than May Day in Moscow circa 1983.